Star Trek may have introduced the expression, “to boldly go where no man has gone before,” but we’re the ones who actually get to do it in today’s post. To my knowledge, nobody has ever compared the before- and after-tax returns of Guaranteed Investment Certificate (GIC) ladders versus bond ETFs. At least I’ve not found an unbiased, historical comparison anyplace online.

Until now!

Before we jump into the numbers, let’s take a look at some of the distinct advantages for each, since there’s no reason your portfolio can’t have both GICs and bond ETFs living in happy harmony.

By the way, if you’ve been following me for a while, you may have noticed that none of my model ETF portfolios contain GICs. For simplicity, I’ve only included bond ETFs, mainly because it’s easy to use historical bond index returns to simulate the long-term back-tested performance data. But that doesn’t mean I have anything against GICs. We often include them in our PWL client portfolios.

Advantages of GICs

Shorter maturities. A typical 1–5 year GIC ladder (with an equal investment in each of the ladder’s “rungs” or years) has an average maturity of 3 years [(1 + 2 + 3 + 4 + 5) ÷ 5 = 3 years]. In comparison, the iShares Core Canadian Short Term Bond Index ETF (XSB) has a similar average maturity of just under 3 years – so, there’s comparable term risk.

However, a broad-market bond ETF, like the iShares Core Canadian Universe Bond Index ETF (XBB), has an average maturity of over 10 years. This makes it more vulnerable to interest rate increases than either a short-term bond ETF or a GIC ladder.

No gut-wrenching price drops. Investors hate seeing their “safer” bond ETFs in the red, but “them’s the breaks.” Whether the losses show up due to the premium bond issue discussed below, or increasing interest rates, it’s enough to send conservative investors running for the hills … or worse, into high-dividend-paying stocks.

GICs largely avoid these behavioural issues. Their daily values tick up (never down) due to the money the GIC issuer owes them in the form of accrued interest. If GICs traded on a stock exchange or in a similar secondary market, their daily values would also rise and fall, similar to bond ETFs. Since they don’t, this is really one of those “ignorance is bliss” situations.

No fear of bankruptcy. The Canada Deposit Insurance Corporation (CDIC) covers GICs and other eligible savings up to a maximum of $100,000 in principal and interest – per depositor, per insured category. As long as you stay within these limits, it’s highly unlikely your GIC investment will ever go belly up.

The same cannot be said for some of the bonds in an ETF. Roughly 70% of the underlying bonds in a plain-vanilla Canadian bond ETF like XBB are government-issued, which are unlikely to default. But XBB still invests in about 30% investment grade corporate bonds. While these higher-quality corporate bonds are less likely to default than lower-quality “junk bonds”, the risk is still more than zero.

More tax efficient. Currently, most bond ETFs are chock-full of premium bonds. As the name suggests, you end up paying more to purchase underlying premium bonds than you receive when they mature. This results in a capital loss at maturity. To compensate you for this loss, the bonds pay you extra coupon interest. The catch is, in a taxable account, the interest is taxable at your marginal tax rate, which can result in a higher annual tax bill.

GICs don’t have this premium bond issue. When your GIC matures, you receive your original investment back, plus interest along the way.

Advantages of Bond ETFs

Simpler. It’s easier to purchase one bond ETF instead of managing a multi-GIC ladder. This is especially true if you need to take extra care across many accounts to avoid exceeding the CDIC limits. (That said, you do lose CDIC protection if you invest in a bond ETF instead of GICs)

As a bond ETF investor, you also can set up dividend reinvestment plans (DRIPs) in your funds, to automatically purchase additional ETF shares over time.

More liquid. You can essentially sell bond ETF shares any time, for any purpose, with no repercussions. GICs are typically locked in until their maturity date. You can mitigate this liquidity risk by investing a portion of your portfolio in bond ETFs, for addressing emergency spending needs or to rebalance your portfolio during a stock market meltdown. For more information, see The Most Boring Battle Ever: Bond ETFs or GICs?

Benchmarking fit. Even if a GIC ladder and a bond ETF have comparable long-term expected returns, you’ll likely benchmark, or compare, your yearly fixed income returns to a bond index. A bond ETF’s annual returns will likely closely match its closest bond index annual returns. But a GIC’s return can be substantially better or worse than its closest benchmark from one year to the next – especially during periods of rising (falling) interest rates. If you prefer to closely track a bond index with no surprises along the way, GICs may not be for you.

Higher yields (based on more term risk). This requires a bit more explanation. The best return estimate for a bond or GIC is its yield-to-maturity (YTM). Generally, a ladder of GICs will have a higher YTM than a short-term bond ETF. So usually, a GIC ladder is expected to outperform a short-term bond ETF like XSB.

The YTM on a broad-market bond ETF like XBB can skew higher or lower than a GIC ladder. If you invest in a GIC ladder with a lower YTM than a broad-market bond ETF, you should expect a lower return on your investment … and vice-versa. But keep in mind, when a bond ETF has a higher average maturity than a GIC ladder, you can assume it carries more term risk. In other words, the higher expected return is not a free lunch; it’s compensation for taking more term risk.

For comparison, I’ve included the year-end YTM for XSB, XBB and a GIC ladder, which were available for purchase from National Bank Independent Network (NBIN) over the past seven years. As expected, the GIC ladder had a higher YTM than XSB on each measurement date. XBB generally had higher yields than the GIC ladder, but their rates were fairly comparable in most cases.

Historical YTM: 2011–2018

| Date | XSB | XBB | GIC Ladder |

|---|---|---|---|

| December 30, 2011 | 1.51% | 2.30% | 2.25% |

| December 31, 2012 | 1.59% | 2.29% | 2.04% |

| December 31, 2013 | 1.74% | 2.72% | 2.21% |

| December 31, 2014 | 1.54% | 2.22% | 2.20% |

| December 31, 2015 | 1.20% | 2.01% | 2.01% |

| December 30, 2016 | 1.43% | 2.17% | 1.72% |

| December 29, 2017 | 2.10% | 2.49% | 2.37% |

| December 31, 2018 | 2.37% | 2.73% | 3.15% |

Sources: BlackRock Canada, NBIN

Are We Ready To Boldly Go?

Now that we’ve fueled up our jets with the preliminaries, let’s launch, warp speed ahead, into that cutting-edge comparison I promised – in two parts:

- First, I’ll compare the before- and after-tax returns of XSB vs. a GIC ladder from 2012–2018. As we mentioned earlier, since the YTM on XSB has historically been lower than the GIC ladder, we would expect the GIC ladder to outperform XSB over the measurement period.

- Next, I’ll show you the same analysis of XBB vs. a GIC ladder from 2012–2018. By the way, I chose 2012, because that’s as far back as NBIN has live, historical GIC data. It’s also an interesting starting point. Since the YTMs on a GIC ladder and XBB were very close, at 2.25% and 2.30%, respectively, it indicates we can expect similar future performance.

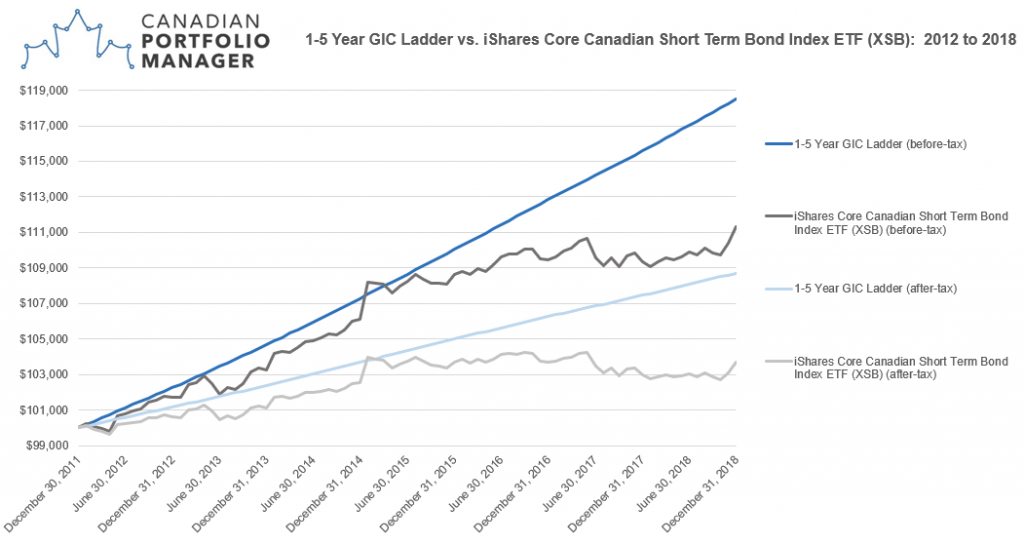

The Big Short: XSB vs. GIC Ladder

So, here are the essentials from our first comparison, starting with $100,000 in each investment and measuring performance from 2012–2018:

- Before-tax, the GIC ladder grew to $118,488, while XSB grew to only $111,331. In percentage terms, the GICs returned 2.45% each year on average, while XSB returned 1.55%, for an annual, before-tax outperformance of 0.90%.

- At the start, the GIC ladder had a weighted average YTM of 2.25%, while XSB’s was 1.51%. Remember, a fixed income holding’s YTM is our best estimate for its future expected before-tax returns. At least in this isolated live-data analysis, the estimate was relatively accurate.

- As expected, XSB had a bumpier ride. As described above, bonds and bond ETFs are priced and can fluctuate in price daily, while the value of a GIC simply increases daily by its accrued interest. This gives GICs that aforementioned “smoother ride” behavioural benefit, even if both, relatively conservative investments arrive at roughly the same place in the end.

- After-tax (assuming the top rate for an Ontario taxpayer), the GIC ladder grew to $108,709, while XSB increased to $103,681. In percentage terms, the GICs returned 1.20% after-tax, while XSB returned 0.52% after-tax, for an annual, after-tax difference of 0.68%.

Key Takeaway #1. If the current YTM of a GIC ladder is similar to or higher than the YTM of a short-term bond ETF, you could consider allocating a portion of your short-term bond allocation to a GIC ladder instead.

Sources: taxtips.ca, BlackRock Canada, cds.ca, NBIN

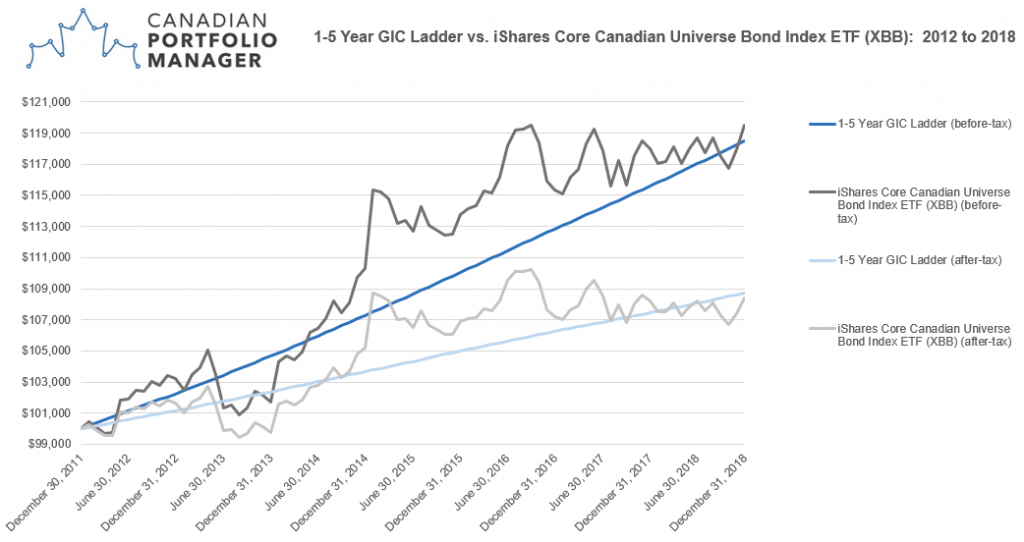

Master of the Bond Universe: XBB vs. GIC Ladder

A GIC ladder arguably behaves more like a short-term bond ETF than a broad-market bond ETF; both GIC ladders and short-term bond ETFs invest in fixed income securities that mature in 1–5 years. A broad-market bond ETF like XBB invests in short-, mid- and long-term bonds, some of which don’t mature for 20+ years. The average maturity of XBB’s bond holdings is around 10 years, while a GIC ladder has an average maturity of just 3 years.

- Before-tax, the GIC ladder grew to $118,488 (just as in our previous example), while XBB grew to $119,525. In percentage terms, the GICs returned 2.45% each year on average, while XBB returned 2.58%, for an annual, before-tax XBB outperformance of 0.13%.

- At the start, the GIC ladder again had a weighted average YTM of 2.25%, while XBB’s was 2.30%. Unlike our first comparison between a GIC ladder and XSB, these initial YTMs were so similar, they make for an interesting analysis.

- It’s worth noting, XBB’s slight outperformance came at the cost of substantial added volatility. In the graph below, you can see many periods where XBB’s value dropped significantly, while the GIC’s market value steadily chugged along. I’ve shown this graph to a number of our PWL clients, who have all pointed to the blue GIC-ladder line saying, “I would rather have that one”.

- After-tax (again assuming the top rate for an Ontario taxpayer), we see a similar story. The GIC ladder managed to squeak ahead by growing to $108,709, while XBB trailed just behind at $108,378. In percentage terms, the GICs returned 1.20% after-tax, while XBB returned 1.16% after-tax, for an annual, after-tax difference of 0.04%.

Key Takeaway #2. If the current YTM of a GIC ladder is similar to or higher than the YTM of a broad-market bond ETF, a GIC ladder is a suitable long-term alternative to a broad-market bond ETF.

Sources: taxtips.ca, BlackRock Canada, cds.ca, NBIN, 2011-2018

Climbing a Logical Ladder

So, there you have it – our groundbreaking comparisons are now complete, which leads to …

Key Takeaway #3. When the YTM of a GIC ladder is similar to or higher than the YTM of a bond ETF, it can be a decent alternative for a short-term or a broad-market bond ETF.

This begs the question: What are those YTMs looking like these days? Ask, and you shall receive:

| Security | Average Yield-To-Maturity (YTM) |

|---|---|

| iShares Core Canadian Short Term Bond Index ETF (XSB) | 1.86% |

| iShares Core Canadian Universe Bond Index ETF (XBB) | 2.19% |

| GIC Ladder | 2.40% |

Sources: BlackRock Canada, NBIN as of June 10, 2019.

As of June 10, 2019, a GIC ladder was yielding more than either a short-term or broad-market bond ETF. If you’ve made it this far, you probably don’t have to be Mr. Spock to conclude: While these conditions persist, it would be reasonable for an investor to decide to swap out some bond ETFs for GICs – especially if they did not require the liquidity, and preferred less ongoing fluctuation in their fixed income investments.

Wow. I thought this was a stellar topic, but it could also leave your head spinning. Please feel free to include any questions in the comments section below.

Thanks for this excellent article, Justin.

Over the last 5 years, I’ve stayed away from Bond ETFs () because the returns – especially exclusive of dividends – have been so poor. I’ve bought GICs instead for fixed income that I don’t need liquid.

If (and I know you won’t predict) IF interest rates are finally rising again, would this analysis between 2011 and 2018 be different? I guess what I’m asking is, aside from liquidity needs, under WHICH CONDITIONS would bond ETFs provide a better return than GICs?

@John Kirkwood – It’s impossible to know when bond ETFs would provide a better return than a 1-5 ladder of GICs, but if the bond ETF had a noticeably higher yield-to-maturity than a GIC ladder, I would expect the bond ETF to outperform over the next 10 years or so (but this would just be an expectation).

ETF is much safer than the GIC because the GIC has only 100k protection, peanuts. The ETF is held at a brokerage firm and while cipf has 1 million protection, the broker usually has even more private insurance on top in the tens of millions. GIC is very unsafe in this sense.

@Justin:You asked in June 2019 “What are those YTMs looking like these days?”. I am guessing it is still the same, if not even better to go with GIC ladder?

I checked the Weighted Average Yield to Maturity for ZAG and its 1.25%. You can get a a 5 year GIC for 1.5%, so does that simply answer the question, that a GIC ladder would best? Would it be a good plan to do this check regularly (at least once a year), and if GIC ladder wins, then take another portion of your Bonds and purchase another 5 year GIC?

Thanks, Que

Actually, if liquidity is important, then one can make a case for bond ETFs over individual bonds. In a cyclical bear market, bond ETF liquidity -especially corporate bond ETF liquidity – can be a significant issue. But at those times, bond ETF liquidity is no worse than the liquidity of the underlying bonds. Bond ETFs have an extra layer of liquidity that individual bonds don’t have, with investors trading bond ETFs between themselves.

This analysis hasn’t gone the attention it deserved.

Your yield with a GIC ladder will likely be greater than with a bond index fund or a short term bond index fund. But to some extent, it should. You’re taking on liquidity risk, and you should get a premium for that. OTOH, with the index funds, you’re taking on some credit risk. This assumes that GICs are somewhat comparable to government of Canada bonds in credit risk.

There are some, for whom the increased return and decreased credit risk of GICs is adequate compensation for the lincreased liquidity risk.. It may come down to what your goals are for investing in fixed income.

In 2019, the Canadian inflation rate was 1.95%. So with the 3 investment products mentioned in the second paragraph, you managed to roughly keep ahead of inflation, but no more. If the higher tax brackets are relevant to your GIC return, you lost money.

I’m primarily a taxable investor. I can’t make money in fixed income. But fixed income can serve a very useful role in risk management. Does owning illiquid fixed income, such as GICs, get in the way of my risk management?

To simplify, I want fixed income primarily to manage the risk of cyclical bear markets. Liquidity in a cyclical bear market is important to me. In that situation, I’m not certain that GICs make sense.

One important advantage of GICs is that they truly are fixed income. With bond index funds, you can make a case that they aren’t fixed income anymore. That certainty of return is gone; you own sluggish stocks instead.

One alternative to a GIC ladder may be a bond ladder. Liquidity would be better.

If you’re going to invest in individual bonds, you want low credit risk, so they would have to be government bonds. IMO, diversification is important , if you’re going to own corporate bonds. And if you want liquidity in a cyclical bear market, you want higher rated government bonds..

Compared to a GIC ladder, a bond ladder is more costly and thus has decreased returns. This is due to the increased transaction costs of bonds compared to GICs. The exception would be if you’re investing a large amount of money in your ladder. In that case, CDIC limits may make a GIC ladder more inconvenient.

Compared to a bond ladder, a GIC ladder can have less reinvestment risk. You can buy GICs where your annual return is reinvested at a known rate. And there is the convenience of automatic reinvestment., which you can’t get with a coupon bond. A strip bond ladder would get around the issue.

The more I think about it, the more I like bond index funds in my situation. The decreased work associated with them is attractive :-).

Hi Justin – circling back to this discussion given the current 0.25% overnight rate. I know nobody can predict the degree or timing of interest rates cuts or hikes, but in this extremely low interest rate environment would you have a preference for XSB vs. XBB in a TFSA/RRSP? And for a taxable account, XSB vs. ZDB?

On a separate note, I do have a part of my funds with a robo-advisor (Wealthsimple) which is pretty heavily weighted in ZFL vs. ZAG. In hindsight this was a great move and I don’t expect for you to know their thinking, but i would hazard to guess that at some point (given today’s rates) it would make since to reduce exposure to long-bonds in favour of those with shorter maturities?

In “normal times” I would prefer to just hold XBB/ZDB and not take a view on rate decisions, but times certainly aren’t normal and would appreciate any thoughts you may have on the matter.

@Darren: I am generally not using short-term bond ETFs, like XSB. For one, the yields are extremely low (around 0.75% after fees). They are also very tax-inefficient when held in a taxable account. If you are concerned about the possibility of rising interest rates, a 1-5 year GIC ladder may be a better alternative, if you don’t require the liquidity.

I really can’t offer any insight into Wealthsimple’s fixed income strategy – you would need to speak with them directly.

Hi Justin,

Are bond etf’s out of whack right now? ZAG, VAB,ZDB.

With the recent equity declines of 20 to 30%. Full 1% interest rate decrease.

The existing broad market bond etf’s from the portfolios should rise in value with the interest rate cuts and damped the equity blows???

What are your thoughts?

thx

TJ

@TJ: As of March 31, 2020, ZAG is up +0.4% year-to-date (while equities are down considerably). Seems like diversification is working as expected.

Justin i have 10K of GICS in an RRSP that just matured. I was thinking of putting it in an ETF (ZGB, long duration gov bonds). Assuming for the near future there is downward pressure on US and Canadian rates there might be slightly more upside potential and liquidity, the latter of which is not critical. Would be you be kind enough to comment?

@Mark: I can’t predict the future of interest rates, so I don’t have anything to add regarding your strategy.

That was a fantastic analysis, great jobs :D

Hi Justin,

Where is better to keep the GICs: in TFSA or RRSP?

Thanks!

@Erika: It would depend on how you’re managing the asset location of your portfolio. If you’re using the traditional approach to asset location, you would hold fixed income securities (like bond ETFs or GICs) in your RRSP first.

Thanks for the quick reply!

I already have bond ETFs in RRSP. But thought to have some GICs in TSFA.

Should I wait to have more room in RRSP to buy GICs there? and use TFSA for equities only?

@Erika: How large are the TFSA and RRSP? If they’re relatively modest, it might make more sense to just buy a bond ETF for your fixed income.

Justin,

They are around 80k together now, with more contribution (aorund 50k) in the coming month’s/year.

In RRSP, I have XBB and want to buy VTI. In TFSA, I thought of buying VEQT or VCN only.

Any suggestions are welcome! thanks!

@Erika: VEQT already includes an allocation to U.S. equities with VUN, so you would be significantly increasing your exposure to U.S. equities if you also held VTI in your RRSP.

At this level of assets, I wouldn’t worry about including GICs or U.S.-listed ETFs in your RRSP. Holding the same asset allocation ETF in both accounts may be a much simpler solution.

I’ll be discussing more about asset location in my upcoming blogs/podcasts, so stay tuned for those!

Excellent. Thanks. I have several times compared XBB to my 5 yr GIC ladder and found the results almost identical. Although my GIC rates are usually a bit higher I think i sacrifice that advantage by delays in placing the rollover money.

Also, isn’t the appropriate comparison to a running ladder where all of the GICs are 5 years with staggered maturities?

@bill rowe: If an investor was adding money to their account, perhaps they would have chosen to purchase just a 5-year GIC at the onset and an additional 5-year GIC each year with their new savings each year (but this wouldn’t have made the analysis as straight-forward, and it would have resulted in a fluctuating average maturity for the GIC ladder at the onset).

Hi Justin,

Bond ETFs (ZDB, VAB) are at market highs. I know I should not market time but does it make zero sense when it comes to bond ETFs in particular?

I already hold a portion I laddered GICs.

@Cameron: If you’re comfortable with your overall asset allocation, I don’t see any reason to attempt a (likely) futile market timing strategy with your bond ETFs. You could consider switching more of your bond ETF allocation to laddered GICs, but this would depend on your personal liquidity requirements and preferences.

Hi Justin,

Assuming a long time horizon, can you comment on the approach you took, assembling a GIC ladder at once vs. only using 5 year GICs and then easing into a GIC ladder over a five year term.

5 years in you would seem to have a similar average maturity. I would imagine yield to maturity to be higher and I’d be interested in both hearing your take and seeing how different the numbers would be if you modeled using historical 5 year rates.

Chris

@Chris: I wouldn’t have been able to run the analysis of easing into a GIC ladder over time, unless there were additional assumptions regarding new contributions (which would have complicated the analysis for these purposes). However, as there would initially be more term risk in the 5-year GIC, it would be expected to have a higher return that the 1-5 year GIC ladder (the 5-year GIC at the start of the measurement period was yielding 2.71%).

If I allocate 20% to bonds? What percentage would you put in a bond etf and what percentage in a gic?

@Pete: I’ve written a blog post on this exact question (it’s meant to be a guideline only – you’ll have to adjust the split for your own circumstances):

https://canadianportfoliomanagerblog.com/the-most-boring-battle-ever-bond-etfs-or-gics/

Justin

Thanks as usual for your brilliant analysis and laying it out in an easy to understand format. Can you for the benefit of your readers actually quantify the actual percentage of taxation in a bond etf for someone in Ontario in the highest tax bracket, given the premium bond taxation issue. I read somewhere that it’s something like 68% or there about,one needs to calculate the price of the bond etf and use excel price function etc, all of which I am not familiar with. I’d appreciate if you can quantify and elaborate on that in your usual, methodical teacher like approach in your blog

Thanks in advance

Lyndon

@Lyndon: Using the historical data we already have from this blog post, if we subtract XBB’s after-tax return from its before-tax return, and then divide it by it’s after-tax return, we end up with a tax rate of 55.04% [(2.58% – 1.16%)/2.58%].

Now, over half of this historical period occurred when the top Ontario tax rate was between 47.97%-49.53%, so this estimate could be understated by a few percentage points.

Justin. Thank you for an excellent analysis. Does anyone use a ladder of stripped bonds anymore in their fixed income holdings?

@Tim Dengate: Tracking the annual tax implications of a ladder of strip bonds is a bit of a pain. When BXF was released (and then ZDB), I think most investors just switched to those ETFs, which provide T3 tax slip reporting for the income.

Excellent article Justin. One more in a great series you’ve been publishing over recent months. As a retired senior, collecting only OAS and CPP monthly but with a reasonable RSP balance, the fixed income side of our asset mix is understandably substantial. So how to invest it wisely but appropriately is a subject I have grappled with for some time. Far more attention in articles is typically focused on equity investing versus fixed income investing so your current article is particularly welcome.. And I’m pleased your article endorses what I have found and have been doing for several years now, ie mixing GICs with Bond ETFs. As you correctly point out GICs give certainty whereas ETFs provide liquidity and sometimes a little better return, especially in an RSP or RIF account. Since FI returns are pretty crappy no matter which investment option chosen, I’ve been accepting the added risk and potential reward of owning some ZCB in lieu of ZAG. Within our overall net worth which substantially comprises our RSPs plus our home (which is a big chunk of our net worth but not very liquid), the added risk of ZCB versus ZAG is something I can live with and still sleep at nights.

@Bob Clark: Thank you for sharing your experience with the GIC + bond ETF combo in retirement.

Hi Justin, thanks for the research that went into this post.

One additional thing regarding bond funds vs. GICs is that bonds have a more negative correlation with equities than GICs do. This can either benefit or harm you in terms of absolute return depending on how the market moves, but holding bonds will reduce overall portfolio volatility more than equities+GICs will.

@Tim: This is a very good point that I should have mentioned – thanks for pointing it out.

I am thinking of investing in xsb to park money instead of high interest savings account yielding 1.5%

Will appreciate comments

Thanks in advance

@Bijoy SAHA: It depends on when you need the cash. If you’re unsure, an investment savings account is generally more appropriate (as it will not fluctuate in value). XSB could lose value over the next few years (or return less than 1.5%) if bond yields were to increase.

You could also check out cashable GICs, and see if they would be appropriate for your situation.

Nothing like real regression and hard data! Thanks Justin, really well done.

@Rob Steele: Glad you liked it!

Is there a typo in key takeaway #3? I don’t understand #3 at all

@Brian: Key takeaway #3 is just combining the first two key takeaways.

Wow! With all the ground-breaking articles you’ve provided, this may serve to be among the very best. The baffling roller-coaster interest rate environment makes for great confusion for fixed income choices in taxable accounts.

BMO’s website shows the ZDB discount bond ETF at 2.08% YTM maturity today. Given the current values you’ve shown, can you speculate on the same takeaway for this category, on an after-tax basis, i.e. current YTM on GICs favours this ladder over the ETF categories?

You’ve commented back to me and others that the strategy to substitute dividend equities over fixed income is wrong — not just for the asset allocation risk change. When you say that the index ETF provides a 3% yield without focus on dividend-focus, I refer to the Vanguard VCN value of 2.55% and Invesco Dividend ETF (PDC) at 4.97%.

Buy & hold investors in the G&M disregard market price fluctuations and cite dividend and dividend growth as the way to go for tax-friendly income in lieu of fixed-income. Can you elaborate on why this is a bad approach?

@Davie215: Thanks! I would say that ZDB is expected to be slightly more tax efficient than ZAG/XBB/VAB going forward, and have roughly equivalent tax efficiency to a GIC ladder. So if a GIC ladder currently has a higher yield than ZDB, it deserves some consideration in a portfolio.

When I quoted the 3% figure, it came from the gross dividend yield available on the most recent index fact sheet for the FTSE Canada All Cap Index (or the S&P/TSX Capped Composite Index) minus 0.06% ETF fees.

Your overall asset allocation (equities vs. fixed income) is based on a number of personal factors (i.e. your ability, willingness and need to take risk). It sounds like the Buy & Hold Globe and Mail investors have a high willingness to take risk. Whether they’ve thought about their ability or need to take risk is another question.

I need to review more closely when you have time probably tomorrow but thanks also I’ve been watching some of your YouTube videos

Yeah, it’s a long blog post to get through (over 2,000 words). I thought about separating it into two, but changed my mind at the last minute.

I did receive a helpful comment from a reader today though: TLDR (for those of you who are unhip like me, it stands for “too long, didn’t read” ;)

interesting and surprising

may not work for a larger portfolio since I assume you are picking rates from very small institutions

today when I look at Coast Capital rates which is very competitive with all the major banks there is no 2.40% found anywhere in their ladder

in fact the yield range is 1.90% to 2.30% — so it does make me question the validity of this study if the GIC rates have been biased unrealistically upwards by institutions to which most of us have no access

@Erich: The NBIN GIC rates available to me are very similar to the GIC rates available at most discount brokerages. To be even more conservative in my analysis, I assumed that the investor couldn’t “double-up” on any issuers (i.e. if a single issuer had the best 1,2,3,4 and 5 year rates, I only used them for the 5-year rate). Investors may also want to shop around at various institutions for even better rates than at their discount brokerage (so their actual GIC returns could have been even higher than the returns in my analysis over the measurement period).

To your argument, I checked out the top GIC rates available at RBC Direct Investing today, which anyone could have access to (June 12, 2019):

1-Year: Equitable Bank = 2.17%

2-Year: Equitable Bank = 2.31%

3-Year: ICICI Bank = 2.34%

4-Year: Homequity Bank = 2.39%

5-Year: Canadian Tire Bank = 2.47%

Average = 2.34%

Ah, so the historical GIC rate data uses the best 1-5 year GIC rates available through NBIN (previously known as NBCN, which I preferred myself), and those rates are the best 1-5 year GIC rates that RBC Direct Investing has on offer, correct?

I guess I really shouldn’t be surprised by this data, as I had expected to a GIC ladder to outperform. I guess I’d maybe expected the after-tax return to be a little better on XBB when factoring in the capital loss that can offset future capital gains, though I’m not sure an easy way to calculate that. That’s getting pretty hypothetical. ZDB would definitely be more tax-efficient.

One added benefit to XBB/XSB is the rebalancing potential. Unless you have your rebalance date aligned with your GIC maturities, it’s very difficult to pull some of your matured GICs when your equity portion was declined.

If one doesn’t mind holding their GICs in a direct-to-consumer bank or credit union account, a pre-tax 1-5 year average GIC yield of 2.86% can be added, which would outperform XBB by an even wider margin (Source: https://www.happysavings.ca/rates/). You might be able to edge it up to 3% if you do some legwork up to a northern Ontario credit union, but that’s probably about as best as you could do. And then, you’ve got to factor in transfer out fees (which you might be able to get reimbursed if the transfer value is high enough) and your gas/wear & tear on your vehicle if the Ontario credit union doesn’t offer digital account opening.

Update: Just checked Windsor Family Credit Union’s Omnia Direct online division: 1-5 year average GIC yield (pre-tax) is 2.85%, so Sunova Credit Union’s Hubert Financial division still beats them by a measly 0.01%. That’d be splitting hairs. ;)

Cheers,

Doug

@Doug Mehus: Correct (the best 1-5 year rates from RBC DI were from today though).

In this analysis, the after-tax returns on XSB and XBB assume that any capital losses realized on liquidation can fully offset capital gains (so this would in turn increase the after-tax value of these bond ETFs).

I mentioned the rebalancing advantage of bond ETFs like XSB and XBB in this blog post (and linked to another blog which details how to mitigate this issue).

You can certainly shop around for higher GIC rates (depending on how much effort you want to exert). I tried to keep this analysis more reasonable for a regular lazy investor to achieve ;)

Thanks, Justin. Indeed, you did mention briefly the rebalancing advantage within the paragraph on the liquidity advantage. Thanks for clarifying how the capital losses factored in to the after-tax returns!

Cheers,

Doug

Thanks for interesting analysis.

Question though, why GIC Ladder YTM is only 2.40%?

If I buy GICs from Oaken for example, I get YTM of 3.05%.

@Vasya: Investors can shop around for better rates for sure. If their portfolio is smaller, they may even be able to buy multiple GICs from the same issuer and still stay within the CDIC limits.

Excellent and thorough post as always, Justin, Thanks. Now, two comments… Since it is possible to get 2.8% on eSaving accounts at present, money up to the CDIC cap might be better in that for now. Next, it should be noted that the CDIC cap is not applicable to provincial cerdit unions. I believe that they enjoy protection by the provincial equivalent, which has a MUCH higher protection limit (as least 250K if I recall). As such, with some credit unions offering good rates, placing larger amounts there might simplify things for some people.

@Ken: Cash at 2.8% would also be an alternative to GICs or bond ETFs (as long as you stay within the CDIC limits).

I tend to stay away from credit unions that are only provincially guaranteed (but that’s just me…I’m a bit of a worrier ;)

That surprises me! So, I take it you wouldn’t also buy higher yielding credit union preference shares (which are not guaranteed by a provincial deposit insurer), redeemable at the discretion of the credit union’s board of directors at par value generally after at least five years?

Presumably, XBB holds some provincial bonds, which would include the Province of Ontario that reportedly has one of the highest per-capita sub-national debts on its books. The Deposit Insurance Corporation of Ontario is a Crown corporation of the Province of Ontario, which is backed by the province. So, the relatively security of DICO deposit insurance and a Province of Ontario bond should be equal. Granted, though, XBB is not 100% invested in Province of Ontario bonds (which is probably a good thing!).

Cheers,

Doug

@Doug Mehus: A credit union preferred share? Absolutely not. I don’t even buy big bank preferred shares.

Agree with you on the bank preferred shares – they’re just too volatile on the downside (without a corresponding upside return!).

Reason why I would potentially like the credit union preferred shares is because they don’t have a secondary market (which adds to their illiquidity), when you redeem them, the credit union buys them back at their par value (what you paid for them). However, because this is subject to when the credit union does another preferred share offering for them to be able to redeem your shares, they are far less liquid. Generally speaking, the major credit unions like Meridian and Alterna Savings (in Ontario) and Sunova (in Manitoba) will usually approve members to redeem up to 20% of their preferred share holdings per year after the initial five year period. Another downside, though not especially significant, is that apparently because credit unions receive preferential corporate income tax rates relative to banks, the federal government does not let them classify their dividends as dividends for the purposes of the dividend tax credit. Thus, the dividend income is treated as interest income.

So, while they’re preferred equity, they behave like a bond (without the downside). The risk is the credit union becomes non-viable and its assets & liabilities are transferred to another credit union or bank, rendering the members’ common and preferred shares worthless. I would say this risk is quite low, but like you said above with respect to investment grade corporate bonds, it’s not zero.

That being said, I don’t own any credit union preferred shares beyond the required minimum (well, that’s not quite true – I do hold $95 additional common shares that pay “dividends” in Sunova Credit Union, but that amount is not significant).

Cheers,

Doug

Hi Justin,

Uh oh. I live in BC and use our local credit union with its unlimited insurance for credit unions CUDIC. Now you are making me think twice about this strategy. I was holding all my fixed income here.

@Emily: Depending on the rates offered by other CDIC insured issuers, it could make sense to consider diversifying your fixed income holdings.

Enjoyed this post Justin. Very clear and easy to understand. Thank you!

@Matt: Glad you enjoyed it, Matt :)

Thank you Justin! Great analysis, truly something I’ve wondered about many times.

@Morgan: Thanks! I’m glad I was able to shed some light on this topic.