Cue ominous action-adventure music: Bah-da-bum-ba-dum (Pause) Bah-da-bum-ba-dum (Pause) … Open to a darkened alley, just past midnight. Chain-linked, foggy, foreboding. You’re all alone. Bah-da-bum-ba-dum (Pause) …

Just a fantasy scene from one of the Terminators? (Five so far, and counting.) Think again. Our own government may not be satisfied with just axing the refundable taxes in a corporation. They also have their sights set on mostly terminating your corporation’s tax-free capital dividends.

You may recall from my past blog that your company’s capital dividend account is where the non-taxable portion of your corporate capital gains are tracked. If there is a positive balance in the account, tax-free dividends can be paid to shareholders.

It’s tax-free now, anyway. Bah-da-bum-ba-dum (Pause) …

If the government’s current proposal is enacted, it will disallow the non-taxable portion of capital gains to be paid out as tax-free capital dividends. They’ll instead effectively tax the “non-taxable” portion of capital gains at the shareholder’s ineligible dividend tax rate when the funds are withdrawn from the corporation.

At first glance, this doesn’t seem fair at all, as individual investors are only taxed on half of their capital gains. Then again, just as in the Terminator series, the good guys and bad guys (and gals) aren’t always immediately obvious. Especially if they’re like Arnold Schwarzenegger and they get reprogrammed between movies.

So what gives? Is there some method to the seeming madness?

The government’s reasons for proposing a tax-free capital dividend ban are similar to why they have proposed eliminating corporate refundable taxes. Small business owners initially pay less tax on their active business income than individual taxpayers do on their regular salary income. It’s as if the government has loaned the small business owner extra cash at 0% interest for investment. So if both types of taxpayers invest their after-tax income in an investment portfolio, the small business owner will end up ahead (due to their initially higher investable income).

By taxing the non-taxable portion of a corporation’s capital gains once it’s distributed to shareholders, the government believes this will rectify the current corporate advantage. Is the new tax form equitable as proposed? Or is it like one of those shape-shifting cyborgs that aren’t what they seem to be? Let’s tear into the numbers and see for ourselves.

Rise of the corporations

In the example below, we’ll once again compare three Ontario taxpayers:

- An individual taxpayer

- A corporation taxed under the current (capital dividend / refund) system

- A corporation taxed under the proposed (no capital dividend / no refund) system

I’ve assumed that the individual earns an additional $100,000 of income. (That is, they are assumed to have already earned $220,000 of other income, so the additional $100,000 is taxed at Ontario’s top personal marginal tax rate of 53.53%.) The after-tax amount of $46,470 [$100,000 × (1 – 53.53%)] is then invested in a portfolio that yields 6% of unrealized capital gains each year. At the end of 10 years, the capital gains are realized, and the 50% taxable portion of capital gains is taxed at 53.53%.

In similar vein, both corporations are assumed to earn $100,000 of active business income, which is initially taxed at Ontario’s small business income tax rate of 15%. The corporate after-tax amount of $85,000 [$100,000 × (1 – 15%)] is then invested in the same sort of portfolio, yielding 6% in annual unrealized capital gains. At the end of 10 years, the capital gains are realized, and the 50% taxable portion of capital gains is taxed at 50.17% (which is the tax rate on passive investment income earned in an Ontario corporation). Any taxable dividends paid from the corporations to their shareholders are then taxed at 45.30% (Ontario’s top personal tax rate for ineligible dividends).

A final caveat: Like a Hollywood producer, I’ve rigged these assumptions a bit to make the calculations easier to follow. Your own, real-life returns probably wouldn’t end in such nice, round numbers.

Judgement day

After 10 years, the individual investor realizes capital gains of $36,751 and pays $9,836 in taxes ($36,751 × 50% × 53.53%), leaving $26,914 of after-tax investment income ($36,751 – $9,836).

The corporation under the current system realizes capital gains of $67,222. Part I federal refundable taxes of $10,308 are paid ($67,222 × 50% × 30.67%) as well as $2,689 of non-refundable taxes ($67,222 × 50% × 8%). Ontario than snags an additional $3,865 of provincial taxes ($67,222 × 50% × 11.50%). This corporation ends the 10-year period with $50,359 of after-tax corporate investment income.

The corporation under the proposed system also realizes capital gains of $67,222 and ends the measurement period with $50,359 of after-tax corporate investment income. Same math then … BUT, under the proposed system, that $10,308 of refundable taxes becomes non-refundable.

After-tax investment income after 10 years (pre-distribution)

| Return on investments in year 10 | Individual | Corporation: Current System | Corporation: Proposed System |

|---|---|---|---|

| Starting portfolio | $46,470 | $85,000 | $85,000 |

| Earn: 6% capital gains each year | $36,751 | $67,222 | $67,222 |

| Deduct: Federal/provincial personal tax | ($9,836) | - | - |

| Deduct: Part I federal tax – refundable | - | ($10,308) | NA |

| Deduct: Part I federal tax – non-refundable | - | ($2,689) | ($12,997) |

| Deduct: Provincial taxes – non-refundable | - | ($3,865) | ($3,865) |

| Equals after-tax investment income | $26,914 | $50,359 | $50,359 |

Hasta la vista, baby

After paying all tax liabilities, the individual investor is left with $73,384 ($46,470 + $26,914).

The current-system corporation is left with a portfolio value of $135,359 at the end of the 10-year period. Once we exclude the non-taxable portion of the $33,611 in capital gains ($67,222 × 50%), and we add back the refundable taxes of $10,308, we end up with $112,057 in taxable dividends available to distribute to shareholders. The shareholders will then pay $50,767 in taxes on these ineligible dividends ($112,057 × 45.30%). They can also receive a tax-free dividend of $33,611, which is the non-taxable portion of the capital gain from the capital dividend account balance.

Once the car-chase scene has ended and the explosions are in a slow burn, corporate shareholders are left with a net worth of $94,901 ($112,057 – $50,767 + $33,611). That’s $21,517 more than the individual taxpayer’s $73,384.

Now let’s look at a corporation under the proposed system. Here too, we’re left with a portfolio value of $135,359 at the end of the 10-year period. But with the termination of refundable taxes and tax-free capital dividend distributions, the entire $135,359 is taxable when it’s distributed as a dividend to shareholders. The shareholders then pay taxes of $61,324 on the ineligible dividends ($135,359 × 45.30%), leaving them with a portfolio value of $74,035 at the end of the 10-year period.

If you’re watching all the action, that’s only $651 more than the individual taxpayer. As you can see, the government’s proposals would get us awfully close to perfect tax integration.

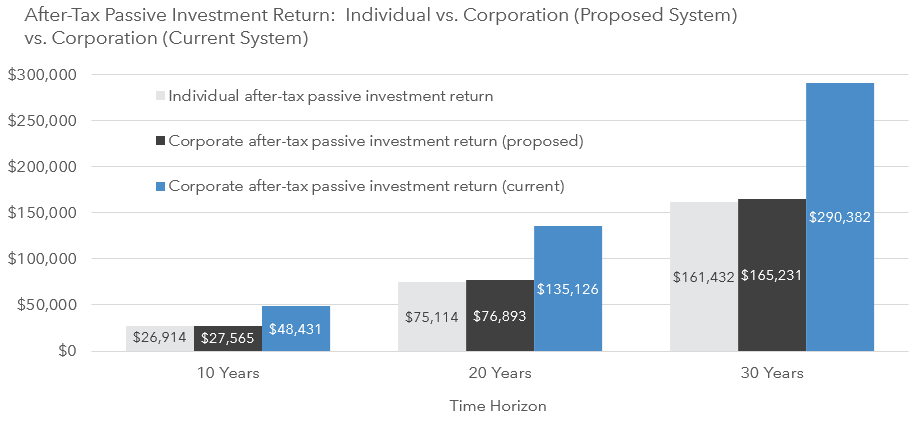

The results are included in the table below (along with an accompanying chart showing the differences over 10, 20 and 30 years).

Net worth after 10 years (post-distribution)

| Individual | Corporation: Current System | Corporation: Proposed System |

|

|---|---|---|---|

| Portfolio value after 10 years | $73,384 | $135,359 | $135,359 |

| Deduct: Non-taxable portion of capital gains | - | ($33,611) | NA |

| Add: Refundable taxes | - | $10,308 | NA |

| Equals: Taxable dividends available to distribute | - | $112,057 | $135,359 |

| Deduct: Personal tax on dividends | - | ($50,767) | ($61,324) |

| Add-back: Non-taxable portion of capital gains | - | $33,611 | NA |

| Equals: Net Worth | $73,384 | $94,901 | $74,035 |

I’ll be back

So, yes, the government has issued a couple of Terminators tasked with killing off two favorable corporate tax breaks. But not unexpectedly, there are those out there staging a Resistance as we speak. I’ll be sure to keep you posted on how any unfolding changes may impact you, your tax planning and your investments.

Bah-da-bum-ba-dum (Pause) …

Thanks for the article!

Great article! Was informative to learn about corporate taxation.

Hi Justin,

I wanted to write a note of thanks for your efforts on this and other series that you make freely available.

Your work and Dan’s work has definitely improved my knowledge of financial and investing topics.

@Erik: Thank you for the kind feedback – it’s nice to hear that our work has made a positive difference for investors.

I’m a Canadian Couch Potato DIY investor who I incorporated 4 years ago. Your detailed analysis on the upcoming tax changes is fantastic. Thank-you!

Once the tax changes are finalized, I would be very interested in an analysis on how this impacts income from different asset types within the corporation. For example – Cdn Equity ETF (Capital Gains and Dividends) vs income from a Bond ETF or GIC’s.

I understand that latest update from the government is that passive income up to 50K in the corporation will be kept under the current tax system. This is something I’m going to have to spend some time getting my head around. For example – does this mean that selling equity to realize capital gains would have to be done over multiple years to keep under the 50K limit?

Anyway… lots of questions and I look forward to your continued posts.

@Chris: Thanks for reading! I’ve already reviewed how the changes could impact earning interest and capital gains in a corporation (I’ll be following up with articles on Canadian eligible dividends and foreign dividend income):

https://www.canadianportfoliomanagerblog.com/corporate-taxation-the-end-of-refundable-taxes/

https://www.canadianportfoliomanagerblog.com/corporate-taxation-terminating-your-tax-free-capital-dividends/

I am also working on a blog that discusses the proposed $50K income threshold. If the corporation’s investment income is below $50K in any year, it may be more tax-efficient to realize a portion of the deferred capital gains in that year (in order to increase the cost base of the securities, and take advantage of the capital dividend account). So “tax gain harvesting” within a corporation will likely be more important than ever before:

https://www.canadianportfoliomanagerblog.com/corporate-taxation-tax-gain-harvesting-crazy-like-a-fox-tax-planning/

I truly appreciate your presentations on this issue. So very helpful.

I have been self employed for 16 years and incorporated 9 years ago. Business has been good as has the stock market, particularly my US Growth ETFs that I purchased when the dollar was at par. I haven’t needed to withdraw half of what I earned for personal expenses and thus have a sizeable portfolio with significant unrealized capital gains. Now what do I do? I am hoping that I get to crystallize my unrealized gains under the current system should the proposal become a reality.

@Brian S: It appears that the government plans to leave any investments that are currently in corporations alone, but we’ll have to wait for the details.

You could always ask your accountant if tax gain harvesting within your corporation could make sense for you: https://www.canadianportfoliomanagerblog.com/corporate-taxation-tax-gain-harvesting-crazy-like-a-fox-tax-planning/

You forgot to add in the salaried employees benefits (medical/mat leave/sick days/vacation/ei/training) which can be in excess of 96000$ AND you forgot to add in the canada and private pensions which will be paid out at retirement which can then be income split. Suddenly the salaried Canadian has pulled ahead financially. You also forgot to subtract medical/mat leave/sick time/unemployment time/equipment costs/ training costs from the incorporation numbers. The old system was “fair”. Fair doesn’t always mean equal. It’s not apples to apples and that is the whole point of the incorporation.

But nice try.

@Louise jarbo: Just trying to educate my readers on how the math works – please feel free to forward your comments to Bill Morneau.