Why do some people still use XEF/XEC vs. VIU/VEE, since both VIU and VEE are more diversified?

As new ETFs are released, it’s natural for index investors to succumb to what I like to call “ETF envy”. I often witness it when an ETF provider lowers their fees below that of their competitors’ – this is usually met with investor excitement as they frantically switch their higher-cost fund to the lower-cost alternative. As one would expect, the higher-cost provider usually follows suit by lowering their fee to match.

This can be detrimental to an investor’s financial health if it causes them to realize unnecessary trading costs, bid-ask spreads and capital gains in pursuit of a temporarily superior product.

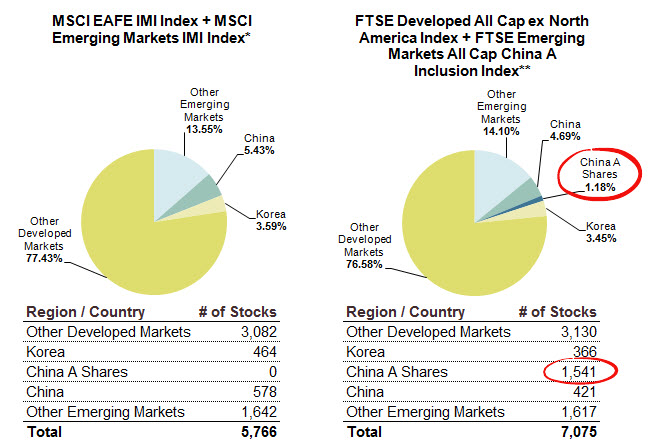

Hard-core index investors also tend to exhibit this behavior while in search of the most diversified ETF. If we base our decision simply on the number of underlying index holdings that an ETF tracks, Vanguard would beat iShares hands down (7,075 stocks vs. 5,766 stocks). However, it is important to dig a little deeper with our analysis to ensure we have not missed any subtleties that may impact our decision.

iShares ETFs

| Asset Class | Security | Commission-Free Account |

|---|---|---|

| Canadian Bonds | iShares Core High Quality Canadian Bond Index ETF (XQB) | $2,122 |

| Canadian Bonds | Vanguard Canadian Aggregate Bond Index ETF (VAB) | $2,618 |

| Canadian Bonds | BMO Aggregate Bond Index ETF (ZAG) | $1,613 |

| Canadian Stocks | iShares Core S&P/TSX Capped Composite Index ETF (XIC) | $2,345 |

| Canadian Stocks | Vanguard FTSE Canada All Cap Index ETF (VCN) | $2,988 |

| Canadian Stocks | BMO s&P/TSX Capped Composite Index ETF (ZCN) | $1,999 |

| US Stocks | shares Core s&P U.S. Total Market Index E?TF (XUU) | $2,190 |

| US Stocks | Vanguard U.S. Total Market Index ETF (VUN) | $4,081 |

| US Stocks | BMO s&P 500 Index ETF (ZSP) | $3,150 |

| International Stocks | iShares Core MSCI EAFE IMI Index ETF (XEF) | $2,646 |

Vanguard ETFs

Corporate Taxation of Active Business Income: Summary

| General Formula | Amount | Calculation |

|---|---|---|

| Base amount of Part I tax | $38,000 | $100,000 × 38% |

| Deduct: Small business deduction | ($17,500) | $100,000 × 17.5% |

| Deduct: Federal tax abatement | ($10,000) | $100,000 × 10% |

| Equals: Part I tax payable | $10,500 | $38,000 - $17,500 - $10,000 |

| Add: Provincial or territorial tax | $4,500 | $100,000 × 4.5% (Ontario) |

| Equals: Total tax payable | $15,000 | $10,500 + $4,500 |

| Remainder: After-tax business income | $85,000 | $100,000 - $15,000 |

The inclusion of China A shares in FTSE indices

In May 2015, FTSE released several new emerging markets indices, which included a modest allocation to China A shares (about 5%). In November 2015, Vanguard began transitioning to these new indices, which currently include an additional 1,541 China A shares.

Although this may sound impressive, the 1,541 additional China A shares account for only 1.18% of the total developed/emerging markets allocation. To put this into perspective, for a balanced Couch Potato portfolio that allocates 20% to VIU/VEE, only 0.24% of your entire portfolio will hold the additional China A shares.

Sources: MSCI and FTSE Index Fact Sheets as of May 31, 2016

*77.43% MSCI EAFE IMI Index + 22.57% MSCI Emerging Markets IMI Index

**80.03% FTSE Developed All Cap ex North America Index + 19.97% FTSE Emerging Markets All Cap China A Inclusion Index

MSCI on a slow boat to China

Although MSCI has not yet added China A shares to their indices, it is only a matter of time until they do (MSCI will be announcing their next China A share inclusion decision on June 15, 2016). MSCI has proposed an initial 5% partial inclusion of China A shares (or about 1.1% of their emerging markets index). If they move ahead with this proposal, it will take effect in June 2017. The initial allocation will be less than the amount FTSE started out with, but will likely include a larger number of stocks (which may in turn make XEF/XEC look more diversified than VIU/VEE).

In the end, there is no right or wrong decision. Both pairs of ETFs will provide adequate diversification for investors. MSCI and FTSE will eventually have a similar allocation to China A shares in their emerging markets indices, so any significant differences in weights or stock holdings is expected to be temporary.

Hi Justin, the first few tables in this blog post seem to have gone haywire while viewing on a mobile device.

Hi Justin,

Amazing work. Keep it up!

On the topic of getting diversification, I was wondering if I could get your view on this.

Paul Merriman, even in his retirement, continues to advocate an approach similar to yours through his podcasts and publications. His model portfolio is summarized here:

http://paulmerriman.com/ultimate-buy-hold-strategy-2016/

Just focusing on the equity side of both yours and his model portfolio, the key difference seems to be his suggestion that in the long-run more heavily weighting a portfolio towards small-cap and towards value leads to significantly higher expected annual returns (which then become over compounding over decades) without a substantial increase in volatility. An example of such a portfolio can be seen in the “aggressive” column here using vanguard as an example:

http://paulmerriman.com/vanguard-tax-deferred-etf-portfolios/

I recognize Paul’s advice is from a US investor perspective and it does add some minor portfolio complexity. So my questions are two part:

1. Do you agree with his conclusions that a better long-term historical returns are achieved by weighing a portfolio towards small-cap and value?

2. If so, how can a Canadian pull off tweaking their portfolio without having the costs of tax inefficiencies, fees and spreads eat up the expected performance benefit? Are there TSE listed ETFs that do the job, or must we look to US listed ETFs and just suffer the extra tax implications?

Thanks!

@Will H: To your first point, I do agree with Paul’s comment that value stocks and small-cap value stocks as a group have outperformed the broad-market over the long term. Whether or not this leads to higher returns going forward would depend on many factors (i.e. how much of the equity component is “tilted” towards small-cap value, costs, taxes, measurement period, investor behaviour, etc.).

In terms of Canadian-listed products that are available, there are many ETFs that tilt towards value, small cap, momentum, profitability, and other risk factors. I have generally recommended that DIY investors keep things simple, and stick to broad-market ETFs instead. In the future, I’ll look at posting more articles about this type of strategy.

What is the minimum to start up this fund Vanguards ETF?

Goolam – there’s no minimum recommended amount to invest in Vanguard’s US-listed ETFs, but you do have to consider the additional complexity and trading costs involved with holding more ETFs (and placing even more trades to implement Norbert’s gambit). I used these particular US-listed ETFs in my example as they were the exact underlying holdings in VXC (so I wanted the comparison to be apples-to-apples). In practice, I tend to use a combination of VUN/VTI, XEF/IEFA, and XEC/IEMG in the portfolios that I manage (which tend to be above $500K).

Is there any value of adding XEC if the invested amount is less than $300k?

As per Vanguard Canada website, the number of holdings of VIU is 2,815 but you mentioned number of stocks in the index is 3,496. I was wondering what is the difference between number of holdings and number of stocks. Thanks!

@WS – for a typical balanced portfolio over $50,000, including XEC could be considered (this figure could be reduced, depending on what you are paying in trading commissions, and how often you trade).

In terms of the discrepancy between VIU’s holdings and the index, VIU is still a relatively new ETF, and continues to add more stocks to its portfolio as it grows. I would expect that these figures should be similar in the near future.

Hi Justin – Thanks for your reply.

I was comparing XEF’s since inception return against XEC’s return but could not figure out why someone would need emerging market in their portfolio. Is there any study where we can find emerging market outperformed or performed equally against developed market in the last 30 to 40 years?

@WS – for what it’s worth, the MSCI Emerging Markets Index returned 10.47% annualized in Canadian dollars since its inception in January 1988. The MSCI EAFE Index returned 5.41% annualized over the same measurement period.